A CEO-Friendly Strategic Guide to Personal and Business Financial Management

Disclaimer: This guide is educational and informational. It provides strategies for debt management and financial planning. It is not financial advice and does not guarantee results. All financial decisions should be made with professional guidance where appropriate.

1. Introduction: The Importance of Financial Discipline

In both personal and professional life, understanding the dynamics of debt is critical. CEOs and investors recognize that financial leverage can accelerate growth but can also endanger sustainability if mismanaged. This guide explores the strategic frameworks necessary to plan for a secure future while avoiding excessive debt.

Debt, when used responsibly, can fund business expansion, investments, or personal growth. However, excessive debt can lead to financial stress, reduced flexibility, and compromised decision-making.

The objective of this guide is to provide a CEO-friendly, structured approach to:

- Assessing your financial position

- Evaluating borrowing decisions

- Implementing risk controls

- Planning for long-term wealth and stability

2. Understanding Debt: The Strategic Perspective

Debt can be classified broadly into:

2.1 Good Debt vs Bad Debt

- Good Debt: Financing that creates value or generates income. Examples include:

- Business expansion loans

- Education or professional development

- Investments with predictable returns

- Bad Debt: Borrowing for consumption without future income benefits. Examples include:

- Excessive credit card debt for lifestyle spending

- High-interest personal loans with no asset creation

Recognizing the difference is fundamental for long-term planning.

2.2 The Cost of Debt

Interest rates, fees, and repayment terms impact overall financial health. From a CEO perspective, consider:

- Debt as a capital allocation decision

- Comparing the cost of debt to expected returns

- Evaluating the risk of over-leverage

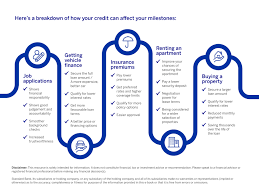

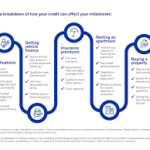

2.3 Debt-to-Income and Debt-to-Asset Ratios

Metrics that provide clarity on financial exposure:

- Debt-to-Income (DTI): Measures your capacity to handle debt payments relative to income.

- Debt-to-Asset (DTA): Assesses how leveraged you are relative to owned assets.

Maintaining healthy ratios ensures flexibility and sustainability.

3. Strategic Financial Planning

3.1 Setting Clear Financial Goals

- Define short-term, medium-term, and long-term objectives

- Align borrowing decisions with measurable goals

- Prioritize financial independence and risk management

3.2 Cash Flow Management

- Regularly track income and expenses

- Maintain an emergency fund equivalent to 3-6 months of essential expenses

- Forecast future cash needs to avoid reactive borrowing

3.3 Budgeting and Capital Allocation

- Allocate capital based on priority: essential obligations, strategic investments, discretionary spending

- Use zero-based budgeting to justify every expense and debt obligation

- Ensure that debt repayments do not compromise essential investments or cash reserves

4. Risk Assessment and Mitigation

4.1 Evaluating Borrowing Risks

Before taking debt, evaluate:

- Interest rates and repayment schedule

- Flexibility of terms

- Impact on operational or personal cash flow

- Contingency plans for unexpected scenarios

4.2 Building Safety Margins

- Maintain liquidity buffers

- Avoid debt commitments exceeding manageable portions of income or cash reserves

- Diversify income sources to reduce dependence on borrowing

4.3 Scenario Planning

Use stress testing to simulate scenarios such as:

- Loss of income

- Rising interest rates

- Market downturns

This allows informed decisions and prevents overexposure.

5. Debt Reduction Strategies

5.1 Prioritizing High-Interest Debt

- Target high-interest obligations first

- Consolidate debt where appropriate to reduce interest expense

5.2 Structured Repayment Plans

- Use methods like the avalanche or snowball repayment approaches

- Track progress regularly and adjust for changes in income or expenses

5.3 Leveraging Financial Advisors

Professional guidance ensures debt reduction strategies are tailored to personal or business financial structures.

6. Leveraging Debt Responsibly

6.1 Debt as a Growth Tool

Strategically applied debt can support:

- Business expansion

- Capital investments

- Leveraged returns on assets

6.2 Monitoring Leverage Ratios

Regularly review debt exposure relative to income and assets to prevent over-leverage

6.3 Maintaining Flexibility

Avoid long-term debt obligations that limit operational or personal decision-making

7. Financial Education and Continuous Learning

- Stay informed about credit markets, interest rate trends, and economic conditions

- Attend professional finance workshops or webinars

- Encourage a culture of financial literacy for teams or family members

Continuous education prevents common pitfalls and supports strategic decision-making.

8. Integrating Debt Management into Strategic Planning

8.1 Align Debt with Strategic Objectives

Borrowing should always support clear objectives:

- Business growth projects

- Personal wealth-building strategies

- Risk-managed investment opportunities

8.2 Periodic Financial Reviews

Regularly assess debt levels, repayment progress, and alignment with long-term goals

8.3 Risk-Adjusted Decision Making

Make borrowing decisions considering probability of outcomes, interest costs, and operational impact

9. Case Scenarios for CEOs and Professionals

9.1 Personal Debt Management Case

A CEO prioritizes mortgage and high-interest credit card repayment, while strategically using low-interest business loans for expansion.

9.2 Corporate Debt Strategy Case

A small business balances operational loans and strategic capital investments, maintaining cash flow buffers and contingency plans.

9.3 Risk Mitigation Case

A professional investor uses scenario planning to model debt obligations against worst-case market scenarios, maintaining solvency even under stress

10. Tools and Resources for Debt Planning

- Financial dashboards for tracking income, expenses, and debt obligations

- Budgeting software for scenario simulations

- Professional advisors for tailored risk assessment

- Educational platforms to improve financial literacy

11. Psychological Discipline in Debt Management

- Avoid emotional borrowing or reactive decisions

- Maintain strategic focus on long-term goals

- Implement accountability through tracking and periodic reviews

Financial discipline, much like corporate governance, ensures sustainable growth and risk containment.

12. Long-Term Vision: Building Wealth Without Excessive Debt

- Plan investment and spending around strategic objectives

- Maintain healthy liquidity and leverage ratios

- Use debt to enhance value, not to fuel unnecessary consumption

- Build a culture of continuous assessment, learning, and adjustment

13. Conclusion

Understanding how not to get too deep in debt is fundamental to both personal and professional financial success. CEOs, investors, and professionals can benefit from a structured, disciplined, and strategic approach to borrowing, repayment, and long-term planning.

Debt, when managed responsibly, becomes a tool for growth, not a source of risk. By implementing the strategies outlined in this guide—clear goal setting, cash flow management, risk assessment, education, and discipline—any professional can plan their financial future with confidence and resilience.

“Strategic debt management is not about avoiding borrowing altogether—it is about leveraging capital intelligently, controlling risk, and building sustainable wealth.”

Too much debt is what too many of you know about right? Yes, debt can be a killer when it comes to trying to make it financially, in this difficult world that we live in. Making smart choices and being knowledgeable about earning money, saving money, investing money and not getting into too much debt, are important issues of interest that should be noticed much more than they are by many.

Throughout this article I want to discuss with you all some helpful information that could potentially help to prevent you from getting into too much debt early on in your adult life. Many people who are just coming out of high school or college often make the same mistake, they rush right into too many different things that they can not afford to pay for, so they finance or charge it all!

Doing this is what starts this terrible and sometimes painful cycle that is not going to do anything except cause you stress and struggle all throughout life. Knowing and understanding just how serious of a problem this can be is very important and finding out this kind of stuff early on in life can really be very helpful and can save you a great deal of heartache later on in life, when you are working on paying off many of your debts that you have collected over the years, for one thing or another.

Debt can destroy any persons life, so no matter how much money you have or do not have, be aware that without even realizing it quickly enough, debt can begin piling up, and start eating you alive. It is not something that many of us ever plan on having to deal with but unfortunately throughout life, some things do tend to happen that we just simply can not control and often times that unfortunate incident can cost you a substantial amount of money, money that you or nobody else can ever really afford.

It is so very important for everyone to understand early on in life just how difficult your adulthood can be because of uncontrollably rising debts each month. This is why you should always be aware of the fact that it can indeed happen to you, just as with anyone else that you know and if you are aware of all the risks surrounding you then you should most definitely be more prepared in knowing just what to do when and if that time does ever come for you, at any unexpected moment throughout the duration of your life.

Do not let debt be your controller, you control all of your actions and try and be as responsible as ever, whenever it comes to how much and what you decide to spend your hard earned cash on. Knowledge of your financial standing at all times, along with some good judgment, when it comes to spending those finances, will help to ensure that debt crisis’s will never be a part of your life.

Tinggalkan Balasan